Hedging tail risks through capital markets

Enhance solvency using swaps to take advantage immediately post-event

True market turning events might be rare, but you want to be prepared for the potential upside thereafter.

What is true for the specialty (re)insurance industry is also true for the wider capital markets, who have developed many hedging strategies to mitigate tail risks. We believe that swaps and options have as yet untapped uses for insurers too, as they can offer cost effective solutions to mitigate extreme tail risk from major catastrophes and black swan events.

Solvency swaps

Carriers use swaps and options to hedge against major currency and equity markets fluctuations, but a solvency swap has eluded structurers as the reference portfolio, particularly if based on market capitalisation-weighted carriers, would always carry too much basis risk.

However, with the introduction of premium weighted methodologies, such as with the RISX equity index, which proxies Lloyd’s, the reference portfolio aligns far better with targeted event risk, facilitating genuine long term solvency swaps in much the same way as carriers’ long term currency swaps. Crucially, using a relevant index removes moral hazards and is applicable to publicly traded and private carriers.

How the swap works

A carrier swaps a fixed price (in bps per annum) against the excess variable return of a liquid premium-weighted equity index (the ‘RISX’ equity index). For a defined period the index returns are swapped with quarterly true-ups and priced to reflect long term de minimis value.

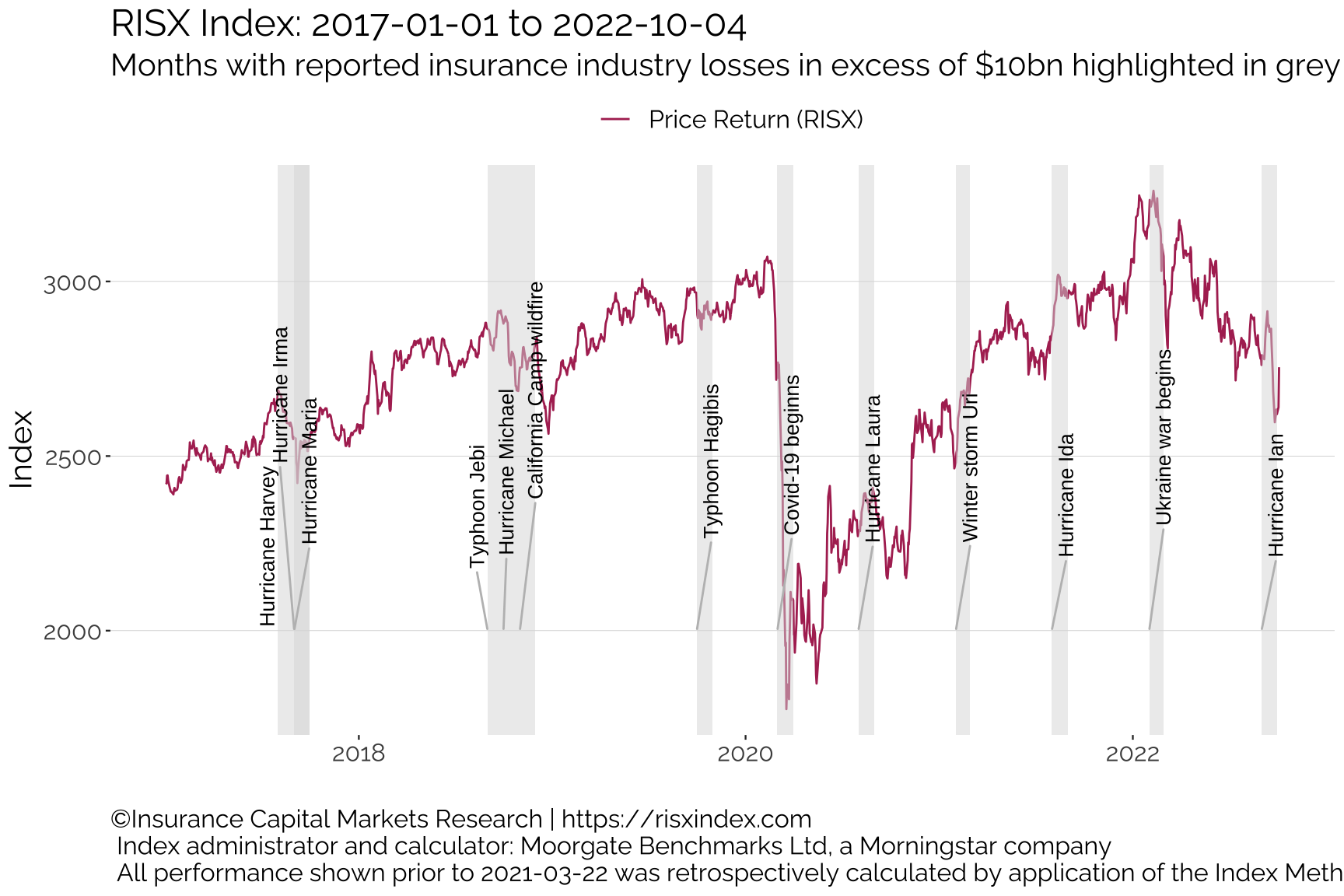

In times of stress following a major global catastrophe event, the index has historically been more likely to lose value in the short term than gain value. In these scenarios, the value of the swap to the carrier will increase in proportion to the reduction in the index. This occurs precisely at the time carriers would want to deploy more capital, not to mention rating agents and regulators increasing their scrutiny of carriers’ financial resources. So swapping the returns of a relevant equity index can enhance a carrier’s solvency and ability to take advantage post-event, giving their senior management confidence and time to manage their post-event response.

The above chart shows the pricing impact of various major Cat events on the RISX equity index going back to 2017. Longer term, the index will tend to return to pre-event levels, hence the long term de minimis pricing.

However, at the critical moment post-event, carriers will immediately have a solvency asset which, depending on size of the event, could be the difference between increasing footprint at a time of very favourable pricing, or not. Furthermore, given the trigger is not event specific, but a catch-all for any scenario, including black swans, such a swap can be the lifeline for survival; to paraphrase Warren Buffet, an instant bathing suit when the tide goes out.

This article was also published as a Viewpoint by The Insurer.