The USD 100bn Secret: How ICMR Calculated Lloyd’s “Market Capitalisation”

Coinciding with the launch of Syndicate Statistics 2026, supported by industry partners Helios Underwriting, Artex Risk Solutions, Peel Hunt, and Milliman

Following Lloyd’s of London reporting a historic £10.6bn pre-tax profit in 2025, the market has rarely looked more attractive. But as a unique, unlisted marketplace, a simple yet critical question often remains unanswered by the broader financial community: What is the Lloyd’s market actually worth?

Alongside the launch of our Syndicate Statistics 2026 book, ICMR has conducted an outside-in valuation analysis. The result? We estimate a notional ‘market capitalisation’ for Lloyd’s of over USD 100bn (£77bn).

If Lloyd’s were a publicly listed company, this valuation would place it as the second-largest financial services entity in the UK, and on the cusp of the top 10 of the FTSE 100 index.

Here is a look under the hood at how we arrived at that figure, and what it means for institutional investors.

The Methodology: The RISX Equity Index

Because Lloyd’s syndicates themselves are unlisted and membership is illiquid, valuing the aggregate market requires a highly accurate capital markets proxy. ICMR created the RISX Equity Index specifically for this purpose.

The index tracks the publicly listed global carriers who own managing agencies within the Lloyd’s market. Crucially, these carriers currently control over two-thirds of Lloyd’s premium and capital. These companies are then weighted to reflect Lloyd’s aggregate risk profile, ensuring the index’s combined ratios and returns on capital closely mimic the market as a whole. The weighting is not as simple as market capitalisation, but instead relates to premium written, and hence risk1.

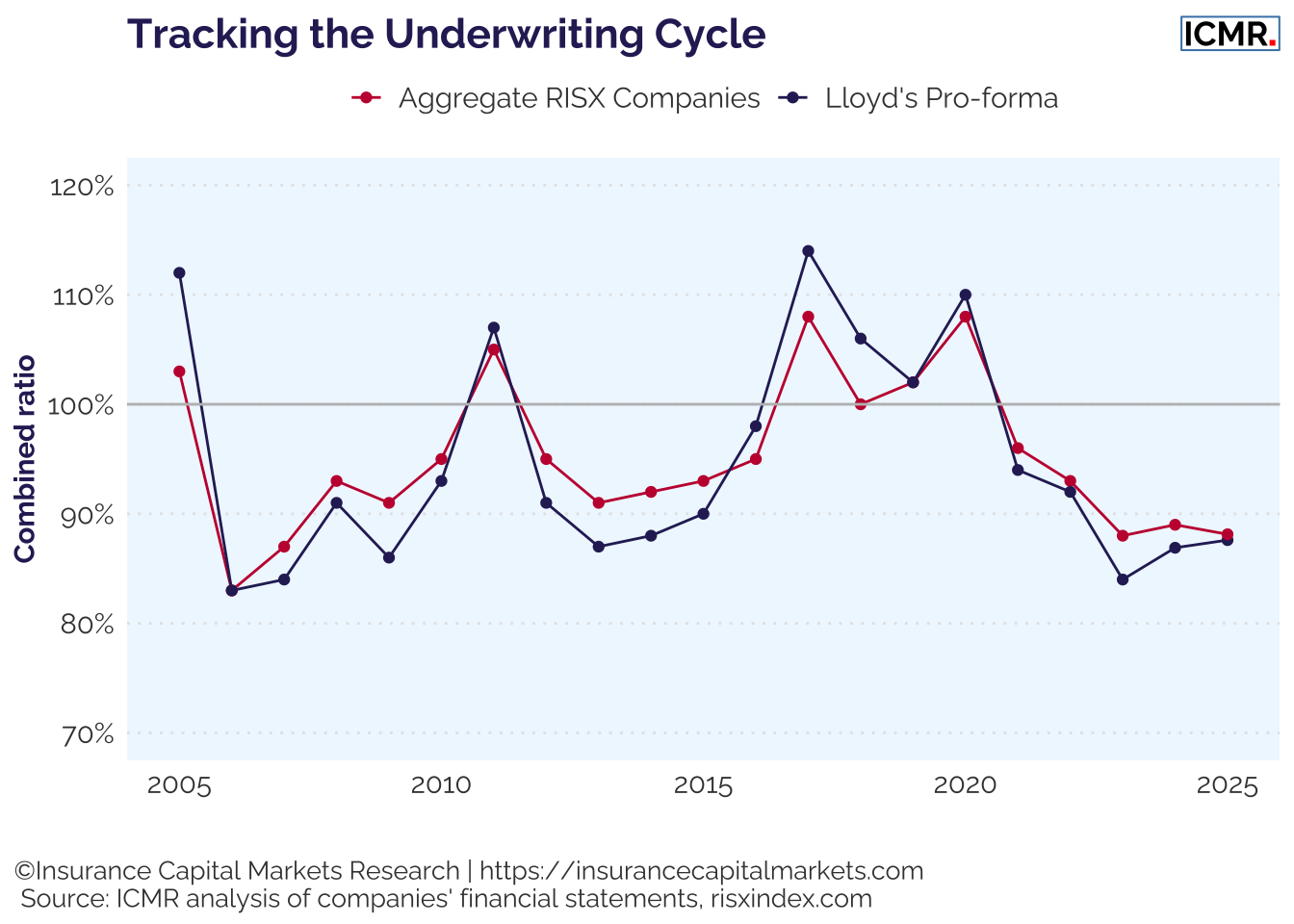

The accuracy of this proxy is battle-tested. Using the RISX Index, ICMR successfully predicted Lloyd’s reported net combined ratio for year-end 2025 almost a full month before Lloyd’s made its official announcement. It has also proven accurate in estimating the value of M&A transactions.

Furthermore, capital markets are pricing this proxy highly. Over the last two calendar years, RISX delivered a 31.8% gain in 2024 and a 22.3% gain in 2025.

The Valuation Math: A 1.65x Multiple, currently

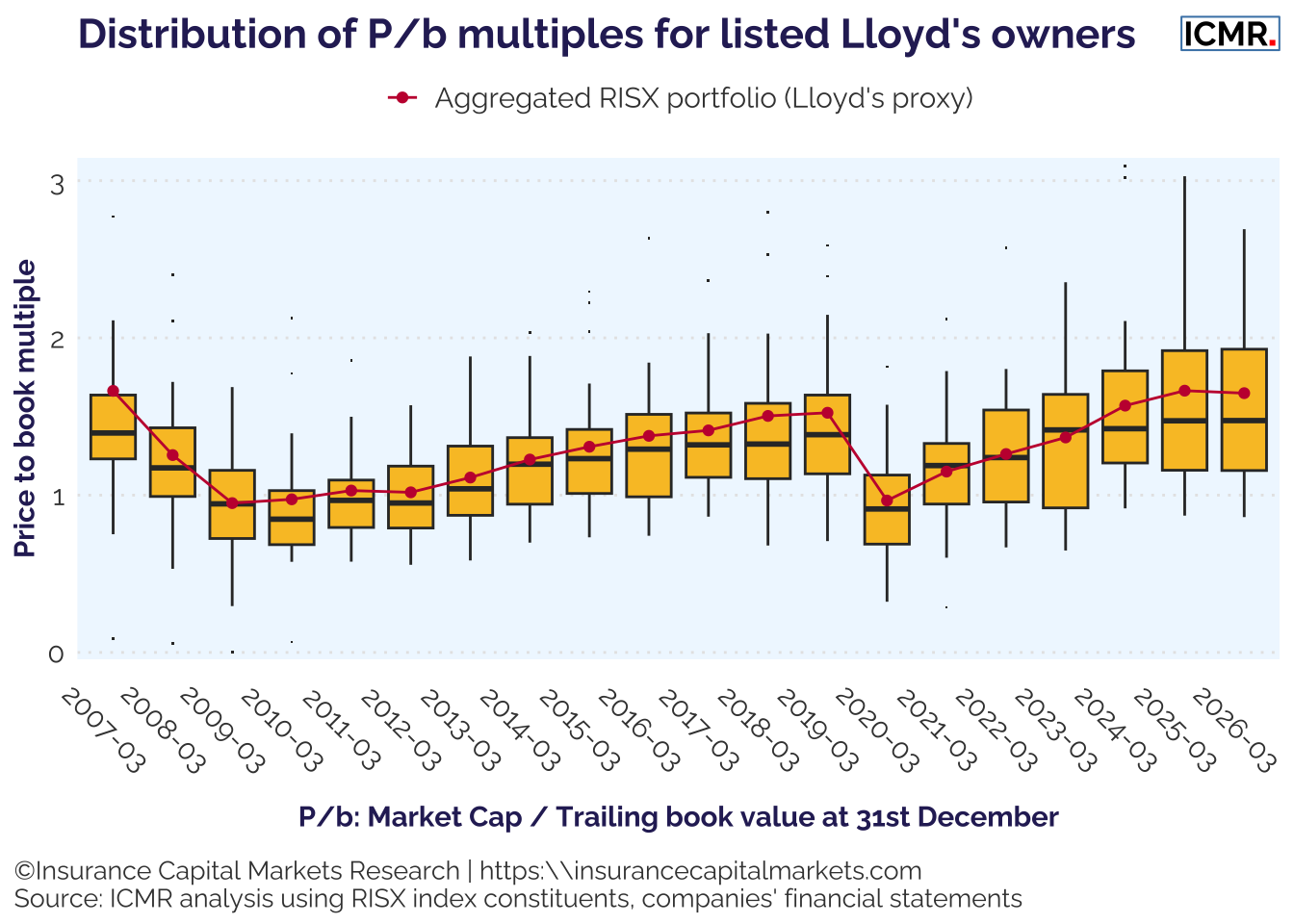

Public market parameters can be observed for each of the RISX constituents, specifically the distributions of price to trailing book values (P/b) at multiple points in time. These distributions and the interquartile ranges within them demonstrate capital markets’ confidence, or otherwise, in sector. Using the RISX weightings gives the capital markets’ valuation on the type of underwriting returns delivered by the Lloyd’s market.

The following chart shows these distributions and interquartile ranges as at Q1 in each year, along with the RISX weighting in red as the proxy for Lloyd’s.

The constituents in the above chart represent over USD 1.1Trn of shareholders’ equity and over USD 1.2Trn of net earned premiums, so it is very much a representative sample. The RISX price to trailing book multiple at the end of Q1 2026 stood at 1.65x book value.

By applying this 1.65x multiple to Lloyd’s total Members’ Assets of £47.1bn2 (our proxy for shareholders’ equity), this makes the notional ‘market capitalisation’ over £77bn, or USD 100bn.

From Macro Valuations to Micro Opportunities

Understanding that Lloyd’s is a USD 100bn economic powerhouse is vital context. However, for institutional capital looking to deploy funds efficiently into the market, macro valuations are only the starting point.

The reality of the “Investor Experience” at Lloyd’s is that finding the right entry points can be complex, and new capital often faces a sluggish timeline to reach full deployment. To bridge this gap, investors need granular, syndicate-level data to identify true “Value Creators” and manage their portfolios actively.

This is exactly why ICMR publishes our annual Syndicate Statistics book.

Syndicate Statistics 2026 provides an aggregate market overview as well as definitive two-page financial and performance analyses for every active syndicate in the market, breaking down performance at both the whole account and class of business levels.

We are proud to launch this year’s edition with the support of our industry partners Helios Underwriting PLC, Artex Risk Solutions, and Peel Hunt LLP, as well as featuring a deep-dive analysis on current market reserving trends from Milliman.

Ready to move beyond the macro headlines? Click here to purchase the full Syndicate Statistics 2026 hard-copy book.

For more information about the RISX index, including Factsheet, White Paper and methodology visit risxindex.com

Footnotes

For more details see the methodology document: https://risxindex.com/downloads/ICMR-ReInsurance-Specialty-Index-Methodology.pdf↩︎

Source: Lloyd’s Annual Report 2025↩︎