Specialty Insurance: A Multi-Asset Approach to a Global Sector

Navigating the ‘Three Plus Three’ Liquidity Challenge through a Multi-Asset Barbell Strategy.

Executive Summary: Navigating the Specialty Cycle

- The “Three Plus Three” Challenge: Traditional Lloyd’s entry faces a dual-ended liquidity bottleneck—three years to reach full capital deployment and a minimum three-year run-off to exit.

- The Barbell Solution: A multi-asset strategy, blending liquid allocations with concentrated direct participations, provides more agility deploy into to the sector.

- Data-Driven Selection: In an era of softening market cycles, the integration of liquid beta (RISX) and granular alpha (Syndicate Statistics) allows for “Cycle Selection”—ensuring capital is always deployed in the most efficient part of the value chain.

The recent publication of the ICMR Syndicate Statistics book highlighted a persistent paradox for institutional investors: the Lloyd’s market has arguably never been more attractive, yet accessing it remains a slow and complex process.

Under current Lloyd’s rules, the capital required for Funds at Lloyd’s (FaL) can take up to three years to fully deploy. In an era where capital markets expect agility, this extended timeframe creates a capital drag that can impact the capital efficiency of the early years of an allocation.

Lloyd’s “Three Plus Three” Liquidity Challenge

The deployment dilemma is not just about the front end. Lloyd’s rules create a double-ended liquidity challenge.

- The Ramp-Up: It typically takes three years to fully scale FaL to support a diversified portfolio. During this time, capital is often held in low-yield “buffer” assets, diluting the overall ROC of the specialty insurance allocation.

- The Run-Off: Extracting capital is equally slow. A decision to exit triggers a minimum three-year run-off period to clear the “tail” of underwriting liabilities and finalise a reinsurance to close (RITC).

This “Three Plus Three” reality means that any direct participation on fewer than three years of account is structurally unattractive. Without a liquid component to the portfolio, capital is essentially unproductive during both the ramp-up and the run-off phases.

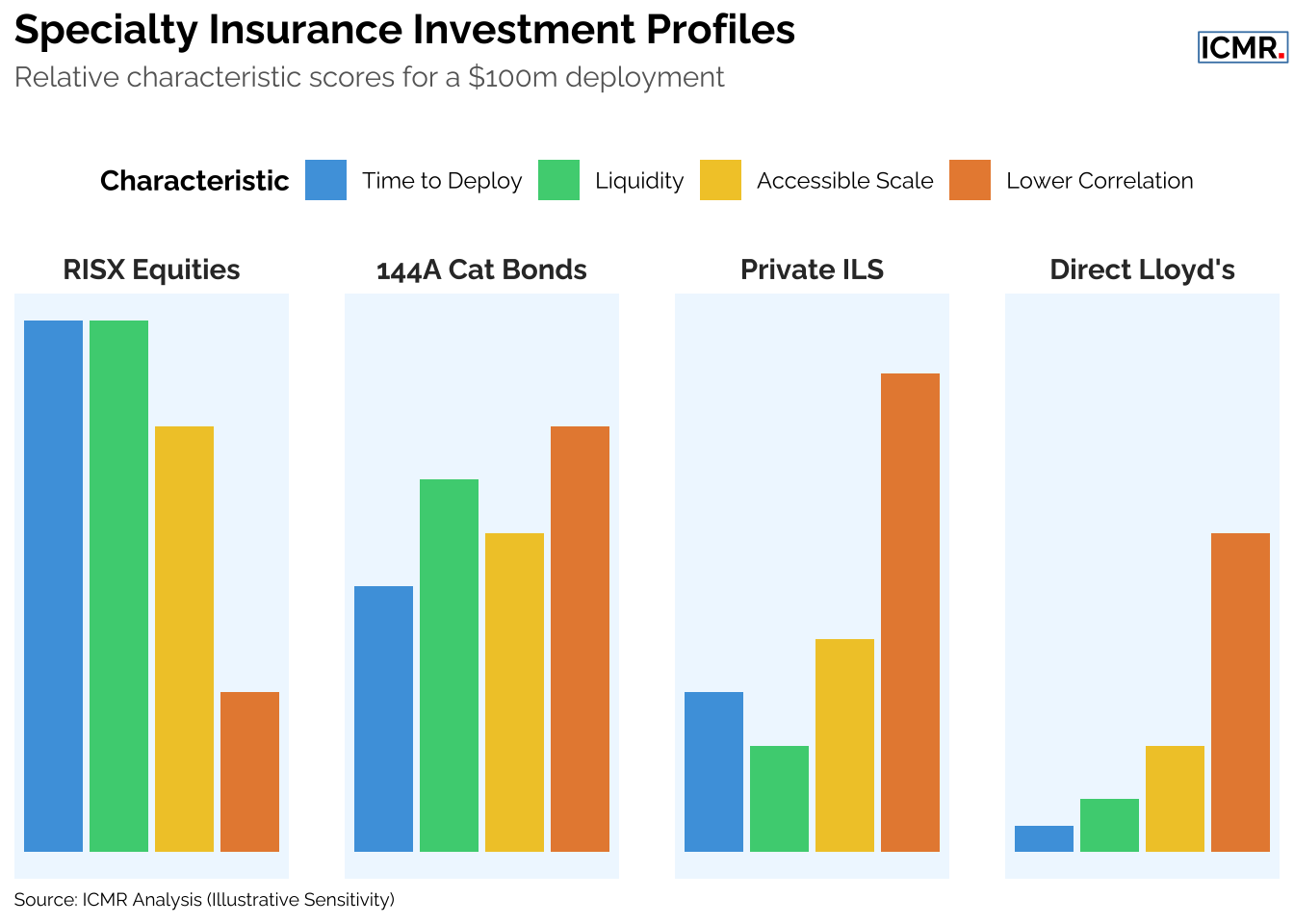

The Barbell Solution: Liquidity as a Risk Management Tool

Bridging this gap starts with viewing Global Specialty Insurance as a versatile asset class with multiple entry points, rather than just a single, slow-moving gate. A “Barbell Approach” allows investors to be productive from Day 1 by blending liquid instruments with direct, long-term underwriting participations.

| Access Point | Asset Type | Liquidity | Primary Benefit |

|---|---|---|---|

| Liquid Equities | RISX Index | High (Daily) | Immediate “Beta” exposure & Exit Agility |

| Public ILS | 144A Cat Bonds | Moderate | Pure catastrophe risk; Low macro-correlation |

| Direct Lloyd’s (FaL) | Syndicate Participation | Very Low | High-alpha access to “Value Creators” |

The “Cost of Waiting” vs. “Correlation Slippage”

The Barbell approach involves distinct trade-offs between different risk profiles.

- The Cost of Waiting: A traditional $100m Lloyd’s allocation that remains partially undeployed for 36 months suffers a “cash drag” that can reduce the internal rate of return (IRR) by several hundred basis points compared to an immediate deployment in the public markets.

- Correlation Slippage: Using the RISX Index as a liquidity proxy introduces “Equity Beta.” While the underlying companies’ earnings are driven by specialty insurance, their stock prices will correlate with broader equity markets during macro shocks. This is the “premium” paid for liquidity.

Furthermore, a liquid leg to a Global Specialty Insurance fund provides the operational flexibility needed to manage the inflows and outflows individual investors.

A Workflow for Capital Deployment

The integration of ICMR’s data tools provides a clear roadmap for navigating this cycle:

- Capture Beta (RISX): Deploy initial capital into RISX Index constituents to capture the market’s current underwriting momentum immediately.

- Select Alpha (Syndicate Statistics): Use the granular performance data in the Syndicate Statistics book to identify the specific “Value Creator” syndicates for long-term participation.

- Tactical Transition: Gradually move capital from the liquid “Barbell” arm into the direct “Alpha” arm as specific opportunities arise, ensuring that every dollar is always earning an insurance-linked return.

The 2026 Shift: Cycle Selection

As the market begins to show signs of softening in certain lines, the ability to pivot becomes a key strategic advantage.

In a softening market, an investor relying solely on a traditional three-year FaL ramp-up risks reaching full deployment just as the cycle peaks. A Barbell strategy allows for Cycle Selection: staying overweight in global diversified equity (RISX) while maintaining exacting standards for which syndicates receive illiquid FaL capital.

Conclusion: Finding the Sweet Spot

The “sweet spot” lies in using liquidity to solve for timing and the “exit challenge,” and using deep data to solve for long-term value. This ensures that capital is consistently deployed in the most efficient part of the cycle, rather than being constrained by structural inertia.

Disclaimer: ICMR is not a regulated financial advisor. This article is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to sell any product. The “Barbell Strategy” and “Three Plus Three” analysis are conceptual frameworks based on historical market observation. Investors should consult with regulated professionals before making capital allocations.