Navigating the Cycle: Why Relative Performance is the Key to Lloyd’s Investment Strategy

Leveraging predictive analytics and alternative capital strategies to maintain profitability as the Lloyd’s market cycle turns.

Executive Summary: Navigating the Specialty Cycle

- The Cycle’s Impact: While recent hard market conditions allowed even bottom-quintile Lloyd’s syndicates to turn a profit, historical data warns that impending soft market conditions will restrict underwriting profitability to only the top half of the market.

- Predictable Performance: ICMR research shows that a syndicate’s relative performance is much more stable—historical top performers consistently stay at the top. Advanced predictive modelling helps investors and smart-follow facilities more reliably identify these consistent winners.

- Modern Market Access: Traditional market entry faces severe liquidity bottlenecks. By adopting a multi-asset “Barbell Strategy,” investors can blend the liquid equity of listed parent companies with concentrated direct capital to top-tier syndicates, offering immediate deployment, better liquidity, and preventing excess capital from suppressing market pricing.

For investors and C-suite executives in the Lloyd’s market, the recent run of exceptional pro-forma results has been a welcome period of profitable trading. However, as capital continues to flow and intense competition begins to drive down rates, the market is undeniably transitioning. While a rising tide lifts all boats during a hard market, the impending softening cycle requires a much more discerning approach to capital allocation and performance measurement.

At Insurance Capital Markets Research (ICMR), our analysis of syndicate data reveals critical insights into how investors can navigate this changing landscape, leveraging relative performance to protect and grow their capital.

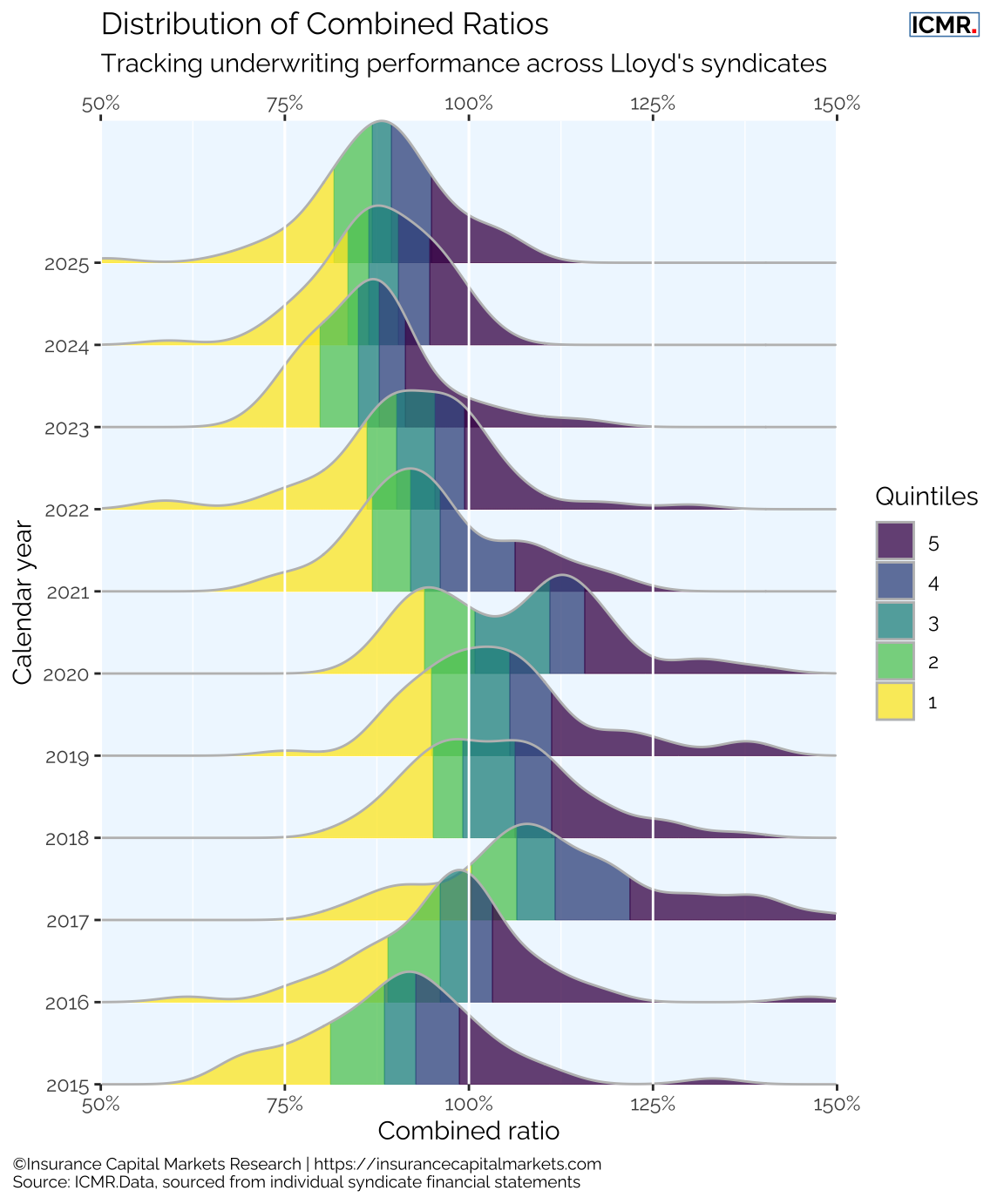

The Reality of the Underwriting Cycle: A Tale of Quintiles

A look at the distribution of combined ratios and net loss ratios across syndicates over the years clearly illustrates the impact of the underwriting cycle. During the recent hard market phase, the rising rate environment meant that the vast majority of syndicates, all the way down to the fifth performance quintile, were able to report combined ratios under 100%.

However, investors must remain vigilant. History shows us that market dynamics shift as pricing softens. Looking back to the last soft cycle, only the top half of the Lloyd’s league table was able to deliver an underwriting profit. Simply participating in the Lloyd’s market is not a guarantee of returns; where you participate becomes the defining factor of success.

Consistency of Relative Performance

If profitability in a soft market is restricted to the top half of the Lloyd’s league table, the critical question becomes: Is syndicate performance purely random?

Our research definitively shows it is not. A syndicate’s relative position in the market is significantly more stable than its absolute performance. When analysing the historical transition frequency for syndicates’ whole account combined ratio performance since 2015, clear patterns emerge:

- Persistent Outperformance: A syndicate in the 1st (top) performance quintile has a 46.2% probability of remaining in the top quintile the following year.

- Persistent Underperformance: Conversely, a 5th (bottom) quintile performer has a 45.7% likelihood of remaining a bottom performer the subsequent year.

- The Squeezed Middle: The greatest preponderance for change from one period to the next falls in the mid-quintiles, where syndicates are most vulnerable to market shifts.

Underwriting outcomes are not entirely random events, as the fortuity of claims does not impact all syndicates equally. Understanding this consistency is the key to developing optimised portfolios.

Predictive Modelling for Strategic Advantage

Recognising the stability of relative performance, ICMR has developed advanced models to predict future relative performance at both a whole account and a class of business level.

This predictive capability provides crucial insight for:

- Follow-Only and Smart-Follow Strategies: Allowing algorithmic underwriting models to index the market efficiently and align with historically consistent top-tier performers.

- Direct Investors: Highlighting the syndicates that genuinely create value over the cycle, allowing capital to be directed away from persistent underperformers before the cycle softens.

Re-evaluating Market Access: The Multi-Asset “Barbell Strategy”

The concentration of top-tier performance raises a strategic question regarding market access. The highest-performing syndicates are notoriously difficult to secure capacity on, and many are fully owned by larger, listed (re)insurance groups. Furthermore, traditional direct participation at Lloyd’s presents a structural “Three Plus Three” liquidity bottleneck for deploying and extracting Funds at Lloyd’s (FaL).

As recently explored in our analysis, Specialty Insurance: A Multi-Asset Approach to a Global Sector, this structural inertia invites a re-evaluation of how to access market returns. Rather than relying solely on direct syndicate participation, our research highlights the potential of a “Barbell Strategy.”

This conceptual framework explores blending highly liquid public market instruments (such as the listed parents tracked by the RISX Index) with concentrated, long-term direct underwriting participations. By examining market access through this multi-asset lens, investors can better understand how to balance liquidity requirements while aiming to capture the returns of top-tier underwriting. Crucially, it demonstrates how allocating to liquid secondary stock, rather than deploying fresh capital directly into the market, might prevent excess capacity from unnecessarily suppressing pricing as the cycle softens.

Leverage ICMR Data to Inform Your Strategy

Whether you are seeking to optimise a portfolio of syndicates or benchmark a managing agency’s performance, transparent, granular data is essential. ICMR provides the definitive tools required for sophisticated capital allocation:

- ICMR.Data: Our foundational dataset cleans, standardises, and models granular syndicate reporting to transform complex information into actionable insights.

- Syndicate Statistics 2026 Book: An indispensable resource for members of the LMA, providing independent assessment and deep-dive analytics into Lloyd’s reported results. Available for purchase on our website.

- The RISX Index: An equity benchmark for the global specialty (re)insurance sector based on publicly listed companies with underwriting subsidiaries at Lloyd’s. It serves as a real-time, liquid proxy for capital markets’ confidence in Lloyd’s-like underwriting returns.

As the market transitions, reliance on prior year momentum will not suffice. Protect your capital by letting data drive your decisions.