Lloyd’s market proxy, RISX, outpaces global benchmarks with 22% total return in 2025

Specialty (re)insurance benchmark shakes off wildfire claims and trade friction

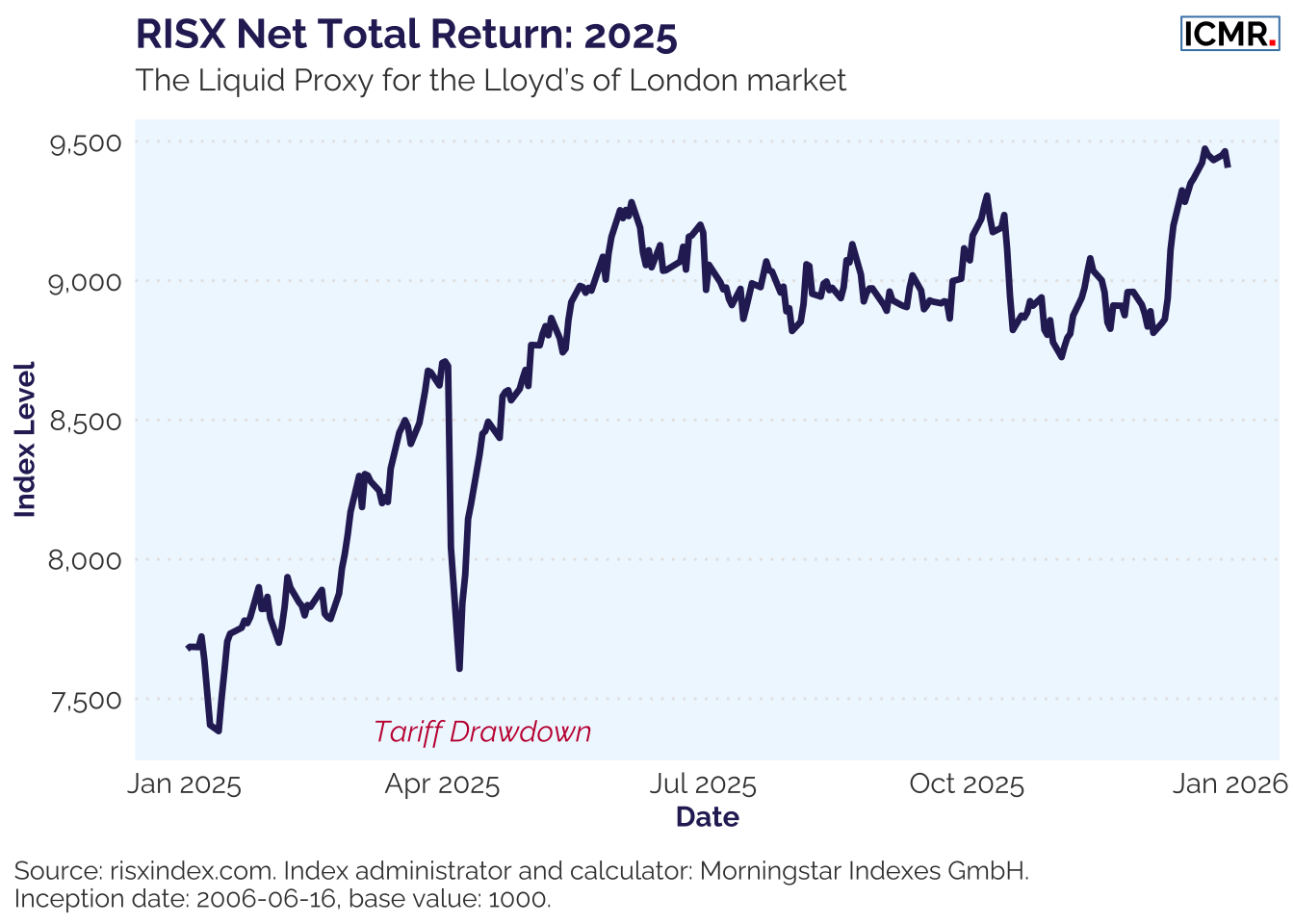

The RISX net total return index, a liquid benchmark for the Lloyd’s of London insurance market, ended 2025 at 9,405 points, capping a resilient year for specialty (re)insurers despite a backdrop of geopolitical volatility, growing trade barriers and another year with catastrophe losses in excess of USD100bn (according to Swiss Re research). This return outperformed major indices, including the MSCI World and the S&P 500. Indeed, the 5 year annualised return statistics are +20%, which exceeds the IRRs of many private equity and specialist hedge funds over the same period.

Navigating seasonal and trade volatility

Investors faced a test early in the year when devastating wildfires hit the Los Angeles area, followed by significant volatility in April with the introduction of new US trade tariffs. This led to the sharpest drawdown over the year, however this “tariff shock” passed notably swiftly, with the index reclaiming all its losses within four weeks.

A relatively benign Atlantic hurricane season provided a tailwind for underwriting margins, allowing the index to climb a further 5 % in December. Throughout the year, the index maintained a consistent dividend yield of 2.13%, suggesting that the index price increases are being backed up by earnings growth, and are not as susceptible to bubbles as, for example, technology stocks.

Comparative returns vs global benchmarks

The 22.3% net total return delivered by RISX was particularly notable when compared to broader equity markets. It outperformed the MSCI World index, which gained 21.3% (NTR USD), and the S&P 500 index of 17.7% (NTR USD).

The lower correlation of RISX with these broader market indices is again illustrated by the different growth periods over the 12 months. This resulted in daily correlation of 30.6% with the S&P 500 and 46.3% with the MSCI World index in 2025.

Corporate restructuring and M&A activity

The year was also marked by a realignment of the index’s 27 company constituent base. Enstar, the legacy specialist, was delisted following its acquisition by Sixth Street. Its place was effectively filled by Aviva, following the UK insurer’s acquisition of Probitas. This was followed by Sompo Holdings’ move to acquire the recently re-listed Aspen Insurance, followed in short order by Skyward Specialty’s acquisition of Apollo Group and Radian Group’s acquisition of Inigo.

Outlook: Renewals and growing demand

As 2026 begins, January 1 renewal reports of softening in the market, particularly in loss free catastrophe business. This coincides with a 9% growth in dedicated reinsurance capital and cat losses sitting 18% below recent averages. Coupling this with falling interest rates may result in tighter margins, however the underlying demand for specialty coverage remains very robust.

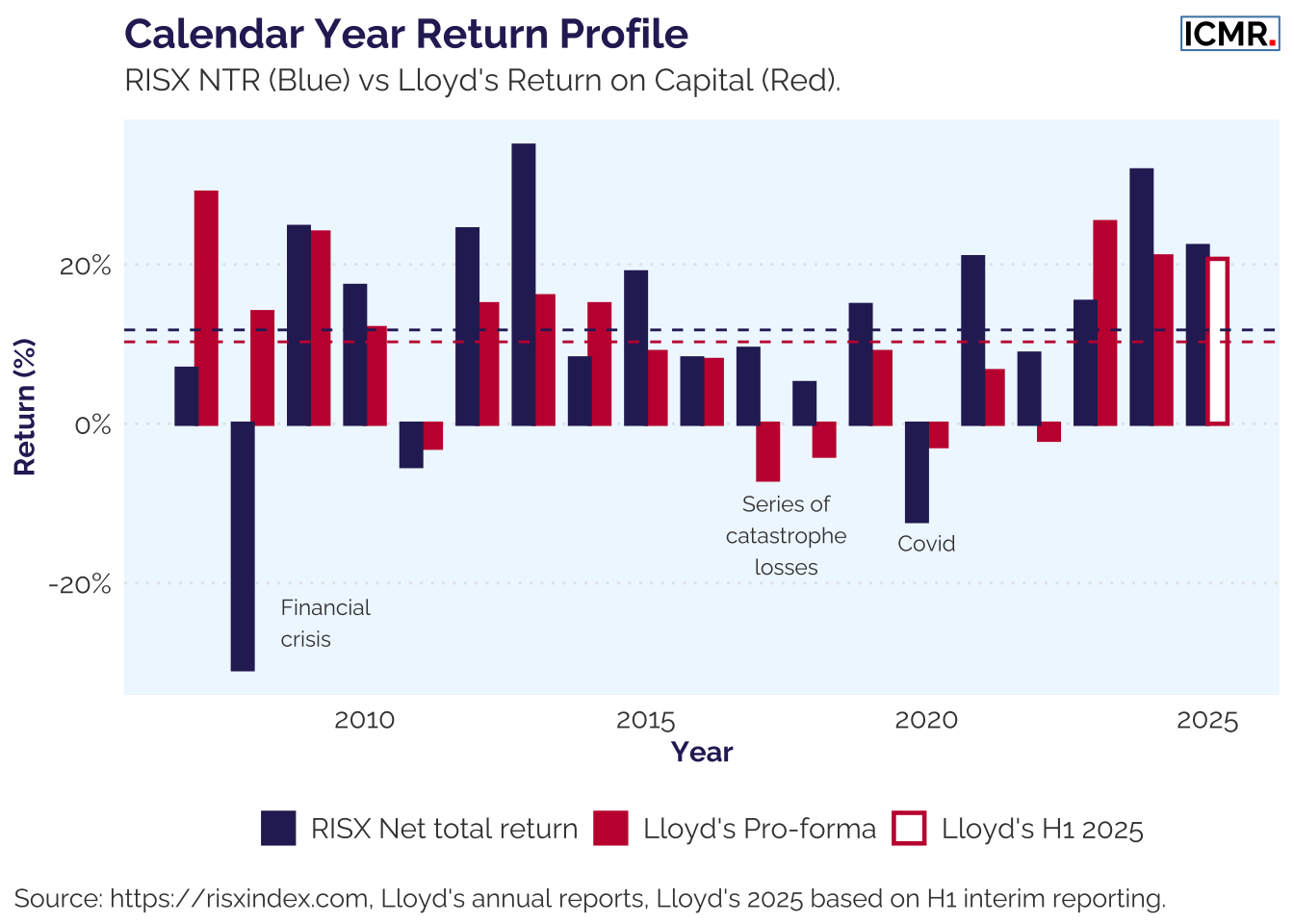

Long term historical returns compare almost identically with Lloyd’s aggregate market returns on capital over the same period (as intended by the design of the equity index methodology).

The above chart highlights this similarity on returns, which is unsurprising as they are both fundamentally driven by the same underlying risk. Incidentally, it also suggests that the likely full year 2025 Lloyd’s market reported return on capital will again be c.20% (20.7% at half-year 2025), comfortably exceeding its cost of capital.

With the current geopolitical and climate landscape increasing the need for sophisticated risk transfer, the constituents of the RISX index continue to enjoy the opportunity to narrow the global insurance gap and address emerging risks.

For more information about the RISX index, including Factsheet, White Paper and methodology visit risxindex.com